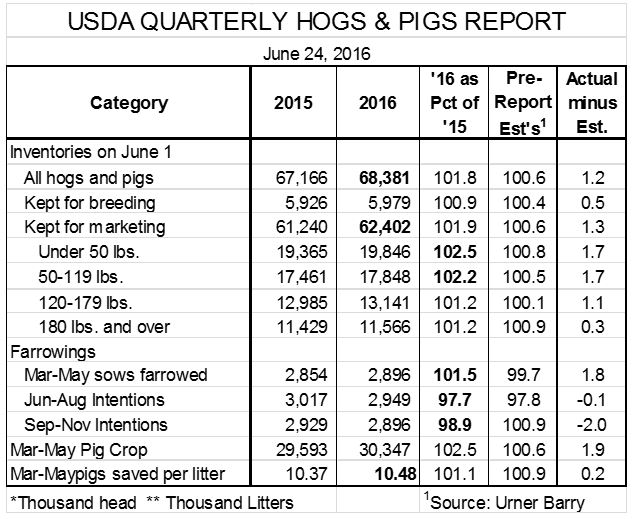

Last Friday USDA released their Quarterly Hogs & Pigs Report which I’ve included along with the Pre-report estimates and so you can see the differences in the far right hand column. You’ll notice that the actual USDA numbers came in quite a bit higher than the estimates across most of the categories. This report is showing that we are going to have more hogs coming to market than what was expected and this has turned the market to a bearish sentiment. Many people (including myself) have been concerned about the number of hogs coming this fall because when compared to our packing capacity it sure looks like we will exceed that capacity for a six to eight week period. Now you look at this Hogs and Pigs report and it is showing an additional 2.5% market hogs for this fall further weighing on this capacity issue.

Last Friday USDA released their Quarterly Hogs & Pigs Report which I’ve included along with the Pre-report estimates and so you can see the differences in the far right hand column. You’ll notice that the actual USDA numbers came in quite a bit higher than the estimates across most of the categories. This report is showing that we are going to have more hogs coming to market than what was expected and this has turned the market to a bearish sentiment. Many people (including myself) have been concerned about the number of hogs coming this fall because when compared to our packing capacity it sure looks like we will exceed that capacity for a six to eight week period. Now you look at this Hogs and Pigs report and it is showing an additional 2.5% market hogs for this fall further weighing on this capacity issue.

The good news is that hog weights are down from last year and I’d guess that this trend will continue at least for the rest of the summer. Right now, August futures for lean hogs are trading roughly $12 / cwt. over October futures where it is historically $9 / cwt. so the market is already pricing in the expectation of having more hogs going into fall.

I would encourage all of our customers to take a look at your expected marketings and develop a strategy to capitalize on the situation in front of us. If you have the opportunity to begin accelerating your hog marketings sooner (starting now) you can capitalize on the higher summer markets. As a result, you’ll take more weight off your hogs allowing you to stay more current heading into the lower fall markets. I don’t need to tell you what happens when we hit the month of September. Hogs start eating new corn and feel the cooler temperatures….weights start to go up and the markets go down! This is why many producers try to do this every year as this is our “normal” seasonal pattern, but I’m stressing it this year because of the current situation where packing capacity in November, December and January are going to be taxed. If we can go into this time frame with lighter average hog weights as an industry, this would definitely help the market situation. This is going to take a concerted effort on your part and I think it would definitely be worth it to your bottom line.

As you have likely heard we have five new packing plants that have been announced and are expected to come on line over the next two to three years. So, once we get through this falls “tight” situation the capacity concerns will be alleviated at least for the next few years. We will see some help yet this fall with two of the smaller plants, Windom, MN and Pleasant Hope, MO coming on line. We don’t know exactly when and how many, but it is estimated that they would add approximately 6,500 shackles per day. Then late next summer / early fall the new larger Sioux City, IA and Coldwater, MI plants will come on line adding another approximately 22,000 / day. Combined these will add 6.2% capacity compared to what we have now! Then we’ll have to see if Sioux City or Coldwater decide to double shift the plants in 2018 or if Prestage gets their plant built in IA in 2018-2019, but if we say that 2 of the 3 happen (which I believe is highly likely) then our capacity will be up around 11% compared to today!

These are huge increases in a relatively short amount of time. As our industry grows this was a necessary step, but I have had many producers tell me that they expect the market to go up significantly once these new plants come on line. My recommendation is to exercise caution. While long term having some new modern packing plants and additional capacity is a good thing, it will take a while for our markets to “absorb” the additional product. Domestic consumption in the U.S. has been flat for 20 years at around 40 lbs. / person so to think consumers here are going to eat the additional tonnage isn’t likely. In my opinion, exports are going to have increase significantly to take most of the increase. This will take time and likely several years to develop. Just because we can slaughter more hogs doesn’t necessarily mean the market is going to go up. At least not until the industry develops market channels to take the additional product.

The good news is that in 2017 slaughter capacity shouldn’t be a limitation for the foreseeable future and packers will have to be more aggressive than the last 5 years in bidding hogs to get their “fair” share. At the same time, producers should be thinking about what they can do to help promote pork worldwide.

For questions, feel free to contact Brian Stevens, President of Big Stone Marketing, at 507.825.7011 or bstevens@bigstonemarketing.com.